It's time to sit back, relax and enjoy a little joe ...

Let's get right to it this week ...

Credits and Debits

Credit: With Labor Day behind us, it's sad to know that some people will always be allergic to work. In South Korea, the desire of some ...

Continue reading Black Coffee: Hi Ho, Hi Ho, It’s Off to Work We Go

Black Coffee: Somebody Is Knocking on the Door, But It’s Not Domino’s

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Let's get right to it this week ...

Continue reading Black Coffee: Somebody Is Knocking on the Door, But It’s Not Domino’s

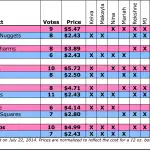

The Average Owner Credit Score and Loan Payment for 10 Popular Cars

In case you missed it, the other day ZeroHedge published a story on the soaring car repossession rate that included some interesting data from Experian comparing the average credit scores and loan payments for owners of ten popular car models. I ...

Continue reading The Average Owner Credit Score and Loan Payment for 10 Popular Cars

Black Coffee: The Quinceanera Edition

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Okay, off we go ...

The Question of ...

Continue reading Black Coffee: The Quinceanera Edition

7 Retaliatory Fees Travelers Should Be Charging the Airlines

One of the greatest technological achievements of the modern era is, unquestionably, the turbine engine. The invention ushered in the jet age, which bestowed upon mankind the luxury of safe and rapid transcontinental and intercontinental travel at ...

Continue reading 7 Retaliatory Fees Travelers Should Be Charging the Airlines

Black Coffee: Sometimes, He Who Sells First Sells Best

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

And away we go ...

Credits and ...

Continue reading Black Coffee: Sometimes, He Who Sells First Sells Best

Black Coffee: More Promises to Pay Tuesday for a Hamburger Today

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Let's get right to it this week ...

Continue reading Black Coffee: More Promises to Pay Tuesday for a Hamburger Today

Pictures of Our $23,922 Bathroom Remodel (and Some Lessons Learned)

After eight weeks, our master bathroom remodel is finally finished. I guess I shouldn't complain; we waited 17 years to make the upgrade. It was also the last room in our modest 2000 square-foot, three-bedroom, two-and-half bathroom home to get a ...

Continue reading Pictures of Our $23,922 Bathroom Remodel (and Some Lessons Learned)

Black Coffee: Neither a Borrower nor a Lender Be

It's time to sit back, relax and enjoy a little joe ...

Let's get right to it this week ...

International News

This past week, I was interviewed by Doug Goldstein for a segment on his terrific money show, Goldstein on Gelt, which is featured on ...

Continue reading Black Coffee: Neither a Borrower nor a Lender Be

Taste-Test Experiment: 11 Kids Evaluate Name-Brand vs. Generic Cereals

When it comes to breakfast, kids can be real cereal killers. Unfortunately, for those of us trying to lower our grocery bill, name-brand cereals can be a very expensive proposition.

That got me thinking: Can kids really tell the difference between ...

Continue reading Taste-Test Experiment: 11 Kids Evaluate Name-Brand vs. Generic Cereals

Black Coffee: Promises, Promises, Promises

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

I planted a couple of tomato plants in the ...

Continue reading Black Coffee: Promises, Promises, Promises

Black Coffee: The Fed, The ECB & the Washington Generals. Winning!

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

We're in the final stages of our ...

Continue reading Black Coffee: The Fed, The ECB & the Washington Generals. Winning!

Black Coffee: You Can Put Lipstick On a Pig — But It’s Still a Pig

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Let's get right to it this week ...

Continue reading Black Coffee: You Can Put Lipstick On a Pig — But It’s Still a Pig

Black Coffee: The Yankee Doodle Dandy Edition

It's time to sit back, relax and enjoy a little joe ...

My dad still gets a kick out of asking people around this time of year if they have a 4th of July in England. Nine times out of ten they look at him like he's nuts and say something like, "Of ...

Continue reading Black Coffee: The Yankee Doodle Dandy Edition

Black Coffee: Why One Billionaire Sees Pitchfork Mobs In Our Future

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Let's get right to it this week ...

Continue reading Black Coffee: Why One Billionaire Sees Pitchfork Mobs In Our Future

Black Coffee: The Summer Solstice Edition

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Summer is finally here. Hooray! I hope ...

Continue reading Black Coffee: The Summer Solstice Edition

How A Lemonade Stand Taught My Daughter To Love Monopolies

Each Father's Day, I love to reminisce about the joys of fatherhood and the days when my teenage kids were younger. This year, I caught myself looking back upon the time several summers ago when my business-savvy daughter, Nina, set up a wildly ...

Continue reading How A Lemonade Stand Taught My Daughter To Love Monopolies

Black Coffee: Friday the 13th, Full Moons & Rising Oil Prices

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Let's get right to it this week ...

Continue reading Black Coffee: Friday the 13th, Full Moons & Rising Oil Prices

Black Coffee: Hokey, Hockey and Horses

It's time to sit back, relax and enjoy a little joe ...

I've been out of town for most of this week, so you know what that means: Yep -- I've got another espresso edition of Black Coffee for you.

Okay, off we go ...

Credits and Debits

Credit: The ...

Continue reading Black Coffee: Hokey, Hockey and Horses

Black Coffee: Kabuki Theater and Ever-Optimistic Markets

It's time to sit back, relax and enjoy a little joe ...

Welcome to another rousing edition of Black Coffee, your off-beat weekly round-up of what's been going on in the world of money and personal finance.

Let's get right to it this week ...

Continue reading Black Coffee: Kabuki Theater and Ever-Optimistic Markets

- « Previous Page

- 1

- …

- 138

- 139

- 140

- 141

- 142

- …

- 152

- Next Page »