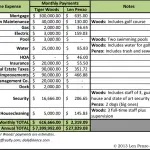

When it comes to holes-in-one, I always tell anyone who will listen that Tiger Woods has got nothing on me.

Did you know I recorded my first ace not long after reaching my 18th birthday, fully two months before Tiger got his first one? I ...

Continue reading Comparing Tiger Woods’ Home Carrying Costs to Mine

What Goes Around Comes Around: Rising Interest Rates Are Inevitable

Last summer my 12-year-old daughter, Nina, was extolling the fashion virtues of her hot pink Converse Chuck Taylor All-Star high-top sneakers, better known to many as simply, "Chucks."

What I found amusing was while Nina really thought she was on ...

Continue reading What Goes Around Comes Around: Rising Interest Rates Are Inevitable

100 Words On: Why Having an Upside Down Mortgage Ain’t All Bad

One of the biggest fears many homeowners have is waking up one day and discovering that they owe more on the mortgage than their house is actually worth. While that may be trouble for those who absolutely positively have to move, it's really no big ...

Continue reading 100 Words On: Why Having an Upside Down Mortgage Ain’t All Bad

If It Feels Good Do It: Maybe Strategic Defaults Aren’t So Bad After All

I bought my first home in 1990 at the top of the Southern California real estate market and promptly found myself with an "underwater" mortgage. And although I owed more than the home was worth over the next seven long years, I never walked away from ...

Continue reading If It Feels Good Do It: Maybe Strategic Defaults Aren’t So Bad After All

Why Marriage Makes It So Hard to Control Remodeling Costs. (Well, Kinda Sorta.)

As I've previously mentioned, the Penzo household is in the middle of a long-awaited home renovation project with a reliable contractor.

Originally, it was supposed to be a fairly modest kitchen renovation that involved replacing our porcelain ...

Continue reading Why Marriage Makes It So Hard to Control Remodeling Costs. (Well, Kinda Sorta.)

Paying Off the Mortgage Early? Not So Fast …

In January 2009 I wrote one of my most popular posts to-date entitled Paying Off Your Mortgage Early Is A No-Brainer. In that post I did a detailed analysis that justified why paying down my mortgage was the right thing to do.

That Was Then, This ...

Continue reading Paying Off the Mortgage Early? Not So Fast …

Using a HELOC as an Alternative to Refinancing

Recently I was talking with a buddy of mine, who happens to be a higher-echelon employee for a major bank, about my desire to refinance into a longer-term home loan in order to provide me with additional financial flexibility in the event I ever lost ...

Continue reading Using a HELOC as an Alternative to Refinancing

Paying Off Your Mortgage Is a No-Brainer

As promised, with our home currently in the process of being refinanced for the fourth time since 1997, I have finished doing an analysis on whether or not to continue prepaying the mortgage early. After running the numbers, I have come to the ...

Continue reading Paying Off Your Mortgage Is a No-Brainer

Got a Fixed Rate Mortgage? Root for High Inflation.

With all the liquidity that the governments of the world have been releasing into the economy, I believe it will only be a matter of time before we begin to experience a nasty bout of inflation that will force interest rates into territory not seen ...

Continue reading Got a Fixed Rate Mortgage? Root for High Inflation.

- « Previous Page

- 1

- …

- 7

- 8

- 9